The Fed’s Problem

The Fed’s Problem Is Not Geopolitics. It Is Transmission.

The market has looked through the geopolitical shock. The problem is that the macro data says the shock is not staying geopolitical.

That is the distinction that matters now. The right instruction is not to trade the war, forecast military outcomes, or turn every oil headline into a rates call. It is to ask whether the U.S. economy is still strong enough for the war’s price effects to travel through energy, freight, supplier deliveries, inventories, business pricing, credit, capex, and financial conditions.

This week’s answer was uncomfortable for the Fed.

The trade flow was not a clean easing market. It was not recessionary enough to justify a confident duration bid, and it was not disinflationary enough to validate the market’s old cut-friendly reflex. It looked much closer to late-cycle nominal resilience with a renewed inflation pulse: activity still positive, labor soft but not broken, price pressure reappearing in business surveys, and financial conditions still loose enough to keep nominal demand alive.

That does not mean the Fed must hike immediately. That is too blunt. The better conclusion is that the distribution has shifted away from hold-or-cut and toward hawkish hold with a live hike tail. The market has repriced some of that. It has not repriced it evenly.

Rates have moved. Risk appetite has not moved enough.

That is the wedge.

The market looked through the war. It may be looking through the wrong thing.

There is a good version and a bad version of “looking through geopolitics.”

The good version is analytical discipline. A macro note should not become a geopolitical forecast. The report should not pretend to know the next escalation path, shipping disruption, diplomatic outcome, or oil supply response. Those are not the variables the Fed controls, and they are not the cleanest basis for portfolio construction.

The bad version is macro complacency. Looking through the event does not mean ignoring the channels through which the event is already entering the economy. If energy costs rise, freight rates move, supplier delivery times lengthen, inventories are rebuilt defensively, and firms start protecting margins through pricing, then the shock is no longer just a headline. It has become transmission.

That is the Fed’s problem. The Fed can look through a headline. It cannot look through a transmission channel if that channel shows up in the same variables it is trying to cool.

The important point is not that the U.S. is booming. It is not. The labor data are soft at the margin. Consumer confidence is not validating a euphoric demand cycle. Some of the manufacturing strength looks defensive rather than organic. The services picture is uneven. This is not a clean acceleration.

But for the Fed, the bar is different. The economy does not need to boom to keep policy constrained. It only needs to remain firm enough that cost shocks pass through rather than disappear.

That is where this week’s data mattered. Manufacturing and services activity were still expanding. Prices paid were elevated. Inventories and supplier delays pointed to defensive ordering and cost protection. Labor was cautious, but not broken. Credit spreads remained tight. Equities were resilient. AI capex remained a meaningful nominal demand support.

That is not the macro mix that invites an easy return to cuts.

This was not an easing-friendly market.

The cleanest way to describe the week is this: growth was firm enough to keep the inflation impulse relevant, but not clean enough to make the Fed comfortable.

ISM manufacturing rose to 54.0, with new orders and production both in expansion. That is not a recession signal. But the same survey had prices paid at 82.1, supplier deliveries still slow, and employment still below 50. In other words, the manufacturing signal was not simply “demand is strong.” It was “nominal activity is firm, but part of that firmness is coming through supply stress, defensive ordering, and price protection.”

Services were even more awkward for a dovish read. ISM services rose to 54.5, with business activity and new orders still solid. But the employment component remained in contraction, while the prices index rose to 71.3. That is a difficult combination for the Fed: services are not collapsing, but labor is cooling and price pressure is still high. It is the kind of mix that keeps policymakers patient at best and hawkish at the margin.

This is why “mixed data” is too lazy as a description. The data are mixed in a very specific way. They are mixed in a way that makes cuts harder, not easier. The weak components are not yet weak enough to dominate the inflation components, while the inflation components are strong enough to prevent the Fed from declaring victory.

The inventory signal matters here. Rising inventories are not automatically bullish. In this environment, inventory rebuilding can mean firms are pulling forward orders because they fear higher costs, slower deliveries, tariffs, shipping disruptions, or energy volatility. That supports near-term activity, but it is not the same as a clean final-demand boom. It is low-quality growth from the Fed’s perspective, because it can preserve nominal activity while refreshing price pressure.

That is exactly the kind of setup where the market can make a sequencing error. If it sees labor softness and assumes cuts are back on, it may be missing the fact that the inflation impulse is being refreshed before labor has broken. If it sees geopolitics and assumes the Fed will look through it, it may be missing the way geopolitics is already moving through business behavior.

The Fed does not need a hot labor market to stay hawkish. It needs inflation to remain too high while labor refuses to crack and financial conditions remain easy. That is much closer to the current setup.

So the market question is no longer whether the Fed can ignore a geopolitical headline. It is whether the Fed can ignore oil, freight, supplier delays, defensive inventories, tight credit spreads, resilient equities, and AI-led capex at the same time. If the U.S. is not in recession, if inflation pressure is being refreshed, and if financial conditions are still too easy, where is the cleanest expression of the Fed’s constraint?

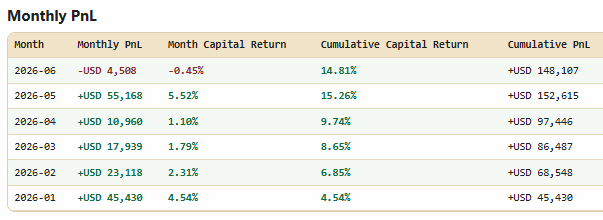

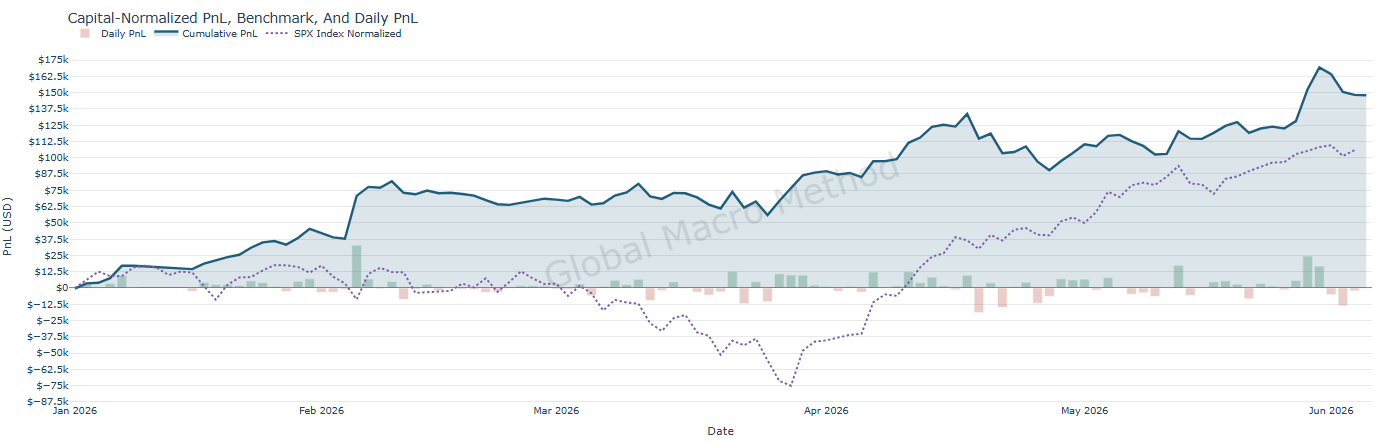

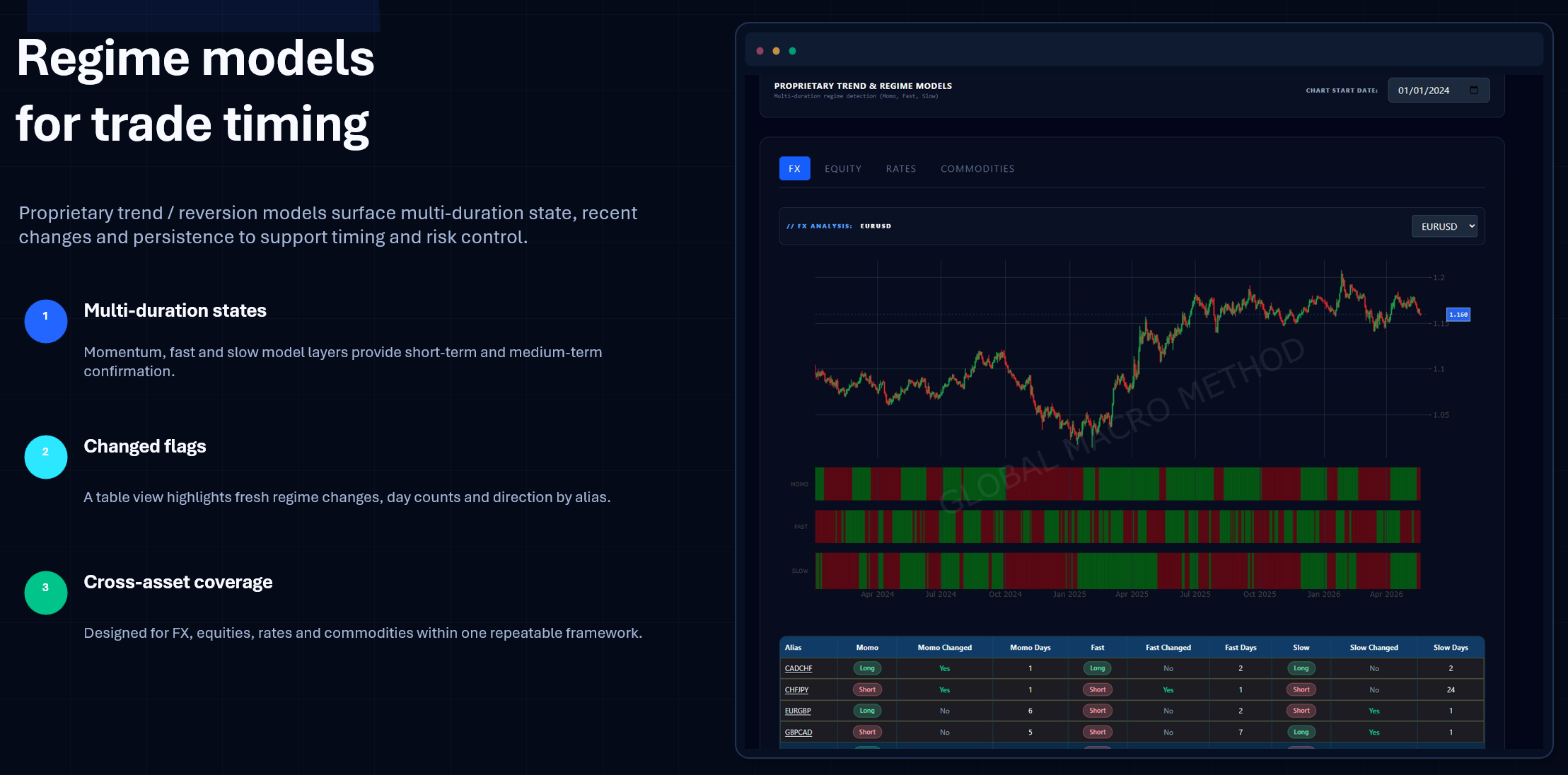

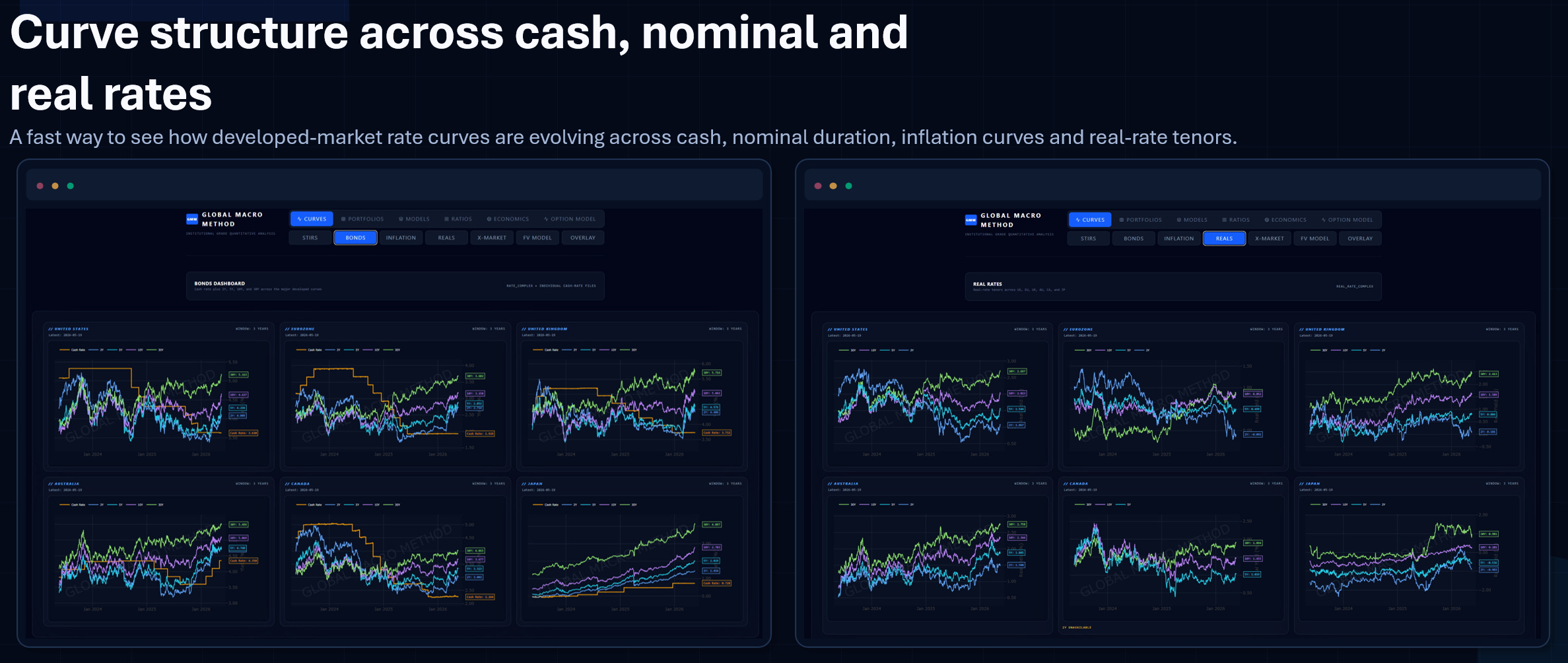

To read more please subscribe. Note all levels of subscription gain access to a bespoke website with curve, models and macro information.

Also the GMM portfolio is performing exceptionally this year, all trades are shared.