Macro Trading Update

Overview & Market Mood

Over the past few weeks, markets have been on a roller coaster. Trade war headlines, fiscal warnings, and central bank surprises have whipsawed sentiment. I’m writing this update to sharing how I saw recent developments and how I’m positioning for the coming week. In short, equities rebounded from an April dip but remain volatile, rates are diverging across regions (U.S. yields spiking even as others cut), commodities tell a tale of two worlds (safe havens up, growth-sensitive ones down), and currencies reflect a softer U.S. dollar with pockets of strength in Europe and Australia. Let’s break it down by asset class and region.

Housekeeping

I'm excited to share my latest tool the daily "Macro Trading Matrix" now available exclusively to my subscribers. This resource provides clear, concise directional bias for key markets, coupled with insightful justifications and reasoning, making it easier to navigate today's challenging market environment.

But this is just the beginning!

Very soon, I'll be enhancing this daily matrix with even deeper insights, including clear target levels, expected value (EV) estimates, and crucial reversal thresholds, helping you identify not just where markets are heading but when to pivot your view.

Additionally, I've completed an advanced analytical framework that leverages options market signals, price action data, machine learning analysis, and AI supported insights to deliver a daily positional bias. This sophisticated tool will significantly upgrade your trading decision-making capabilities, and I can't wait to introduce it to you shortly.

Stay tuned…. big things are coming!

Equities

United States – Tech Rebounds Amid Trade Jitters

U.S. equities enjoyed a strong rebound in early May, led by tech stocks – the Nasdaq surged off the April lows (U.S. equities are up ~22% from those troughs), fueled by optimism around AI and solid corporate earnings. Mega-cap tech has been a bright spot, and frankly I remained overweight tech through this rally, leaning into the AI theme.

However, volatility returned late in the month. Last week saw a mid-week swoon as trade tensions flared: President Trump threatened sweeping tariffs (e.g. a potential “straight 50%” tariff on EU goods by June 1) and Moody’s even cut the U.S. credit rating from Aaa to Aa1. That one-two punch – tariff escalations plus a credit downgrade – spooked markets. The S&P 500 gave back gains on Wednesday and Friday of that week, with selling concentrated in tech: for example, Apple fell ~3% on Friday after fresh tariff threats, and other high-fliers like Alphabet and Nvidia slumped mid-week. From my seat, it felt like a mini replay of 2018’s trade war jitters, with the VIX spiking above 20 again mid-week.

By week’s end, a bit of relief came as Trump postponed the EU tariffs (pushing them to July) – sparking a rebound on Friday. U.S. index futures jumped ~1%+ on that news. Still, markets ended the week on edge. As of now, the S&P 500 is roughly flat-to-up slightly week-over-week, and the Nasdaq is off its highs but still well above April lows. I’m encouraged that U.S. equities have shown resilience – dips keep getting bought – but I’m also hedging more. With key data ahead (notably the Fed’s PCE inflation report on Friday) and big tech earnings (Nvidia’s blowout results are due Wednesday), I expect more swings. I remain bullish long-term on U.S. stocks (strong earnings and structural trends like AI), but near term I’m keeping some protection on, given how sensitive the market is to policy headlines and yields right now.

Canada – Resource Sectors and Tariff Impacts

Canadian equities have largely tracked global trends. The TSX (Canada’s main index) was dragged down during the April sell-off (especially with its heavyweight financials and resource stocks), but it recovered alongside U.S. markets in May. One nuance: Canada initially dodged the worst of Trump’s tariff barrage. The U.S. introduced a baseline 10% tariff on imports, mostly sparing Canada and Mexico under USMCA (with exceptions in autos, steel, aluminum). This “lucky break” meant Canadian exporters avoided some inflationary pain, which was a relief for Canadian markets. In fact, Canadian equities and the loonie outperformed other non-U.S. markets at first, as investors saw Canada as relatively shielded from new tariffs.

That said, Canada isn’t immune. Manufacturing-heavy sectors have been hit by reduced U.S. demand and lingering tariffs on autos/metals. Market sentiment on the TSX soured in early May when the Bank of Canada warned that a prolonged trade war could threaten financial stability, hurting Canadian banks and highly indebted households. I noticed Canadian bank stocks and industrials lagging on those headlines. By late May, as U.S. trade tensions eased slightly and oil prices stabilized (more on oil below), Canadian equities found footing again. The TSX ended last week roughly flat. Going forward, I’m watching Canadian earnings closely – especially in export sectors – for any tariff damage. I’m also mindful that further BoC policy moves (the Bank of Canada meets June 4) could support stocks; if the BoC signals more easing to cushion the economy, that would be bullish for interest-rate-sensitive Canadian sectors (e.g. housing-related stocks). Overall, I have a neutral stance on Canadian equities near term, with a slight positive bias if trade war risks subside.

Europe – Exhaling After Tariff Scare

European stocks have been caught in the crossfire of the U.S. trade saga. Through mid-May, EU equities had actually been performing well – valuations are cheaper than U.S., and we saw investor flows into Europe earlier this year. But the past couple of weeks brought turbulence. Trump’s tariff threats targeted Europe’s exports, hitting autos and luxury goods especially. Last week, the STOXX Europe 50 index fell ~1.9% on Friday alone, with Germany’s DAX down 1.5%, as those sectors sold off. German automakers and French luxury retailers were under heavy pressure when the U.S. was mulling tariffs on European cars and consumer goods. As someone long some European cyclicals, I definitely felt the heat – those positions took a hit on the tariff headlines.

Encouragingly, Europe got a reprieve when Trump backtracked on the immediate tariff deadline. By Monday (May 26), European markets opened higher, recovering some losses. The DAX popped ~1.7% that day. This shows how much Europe’s market was hostage to the trade news – the delay to July 9 gave a short-term all-clear. I’m cautiously optimistic here: Europe might continue to grind higher if worst-case trade outcomes are avoided. Additionally, Europe has a bit of a policy tailwind: the ECB is now in easing mode (more on that in the rates section), which tends to support equities. In fact, European equities have quietly outperformed in some respects, as international investors look for opportunities outside the U.S. tech bubble. I’m keeping some exposure to European stocks, focusing on domestic-demand sectors that benefit from ECB rate cuts and a weaker euro (think European utilities, select industrials). However, I remain careful with export-centric names (autos especially) until there’s clarity on trade negotiations.

Finally, it’s worth noting UK equities briefly: the FTSE was relatively flat (-0.2% on that turbulent Friday). The UK has its own complexities (slower growth, Bank of England cuts, etc.), but since it’s not a focus region here, I’ll just say I’m neutrally positioned on the UK for now.

Japan & Asia – Resilience in Nikkei, China Stimulus Hopes

Japan’s equity market has been surprisingly resilient. The Nikkei 225 mostly shrugged off the global volatility – in fact, it ended that volatile week up (+0.6% on Friday) even as U.S. and Europe fell. Part of this is the yen’s weakness (a boon for Japan’s exporters) and part is Japan-specific optimism. Japanese companies have seen improving earnings and corporate governance reforms, which have attracted foreign investors this year. I’ve been bullish on Japanese stocks for these reasons and have maintained positions there as a diversification. When U.S. markets swooned on trade fears, the classic move would be yen strengthening and Nikkei falling, but this time the yen remained soft and the Nikkei held firm. It suggests that domestic buyers (e.g. Japan’s pension funds) and the still-easy BOJ policy (no drastic tightening yet) are providing a backstop. Going into next week, I’m sticking with my Japanese equity exposure. I do keep one eye on trade talks – Trump’s tariff threats include autos, which could hit Japan hard. If we see any development on U.S.-Japan trade (so far it’s been mostly U.S.-China/EU), I’d reassess. For now, the tailwinds of rising wages and BOJ support make me constructive on Japan’s market.

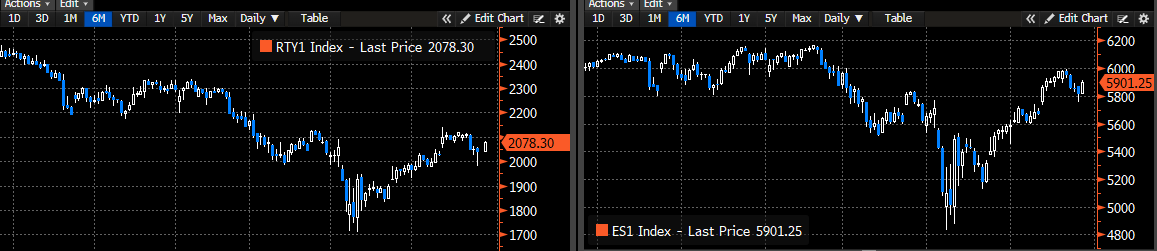

Elsewhere in Asia, China’s stock market actually outperformed recently. Chinese shares rallied on stimulus optimism, as there are rumors Beijing will unveil support measures to counteract the trade war hit. The trade conflict with the U.S. intensified (Trump even dangled the threat of an additional 50% tariff on China if no deal by July), yet Chinese equities gained, anticipating that the government will step in with stimulus (infrastructure spending, rate cuts, etc.). The ripple effect helped Australia’s market too – Australia is tightly linked to China. Even though the ASX 200 saw a sharp correction in March–April (as shown in the chart above), it stabilized and closed flat last week amid the more positive trade tone and China hopes. Australian resource stocks in particular caught a bid on hopes of Chinese demand (iron ore prices have been hovering just under $100/ton). I have a small long position in an Australian equities ETF, as I like that Australia benefits from both Chinese stimulus and its own domestic rate cuts. The ASX recovery has been solid (up ~15% from the April trough as noted). That said, I’m mindful of Australia’s vulnerabilities (housing and consumer spending), so I’m not overexposed.

Bottom line (Equities): Equities globally have regained footing after a trade-induced scare. I remain cautiously bullish. My strategy is to stick with U.S. tech leadership (secular growth stories) but hedge short-term, maintain some European exposure (especially if the eurozone economy perks up with easier policy), and keep Japan/Australia as diversifiers. The coming week, I’ll be watching those key earnings (Nvidia, etc.) and economic data (U.S. core PCE, consumer confidence, China PMI). Any upside surprise there could extend the rally – but any disappointment or new tariff tweet could spark another pullback. Such is life in 2025’s markets!

Rates (Bonds & Central Banks)

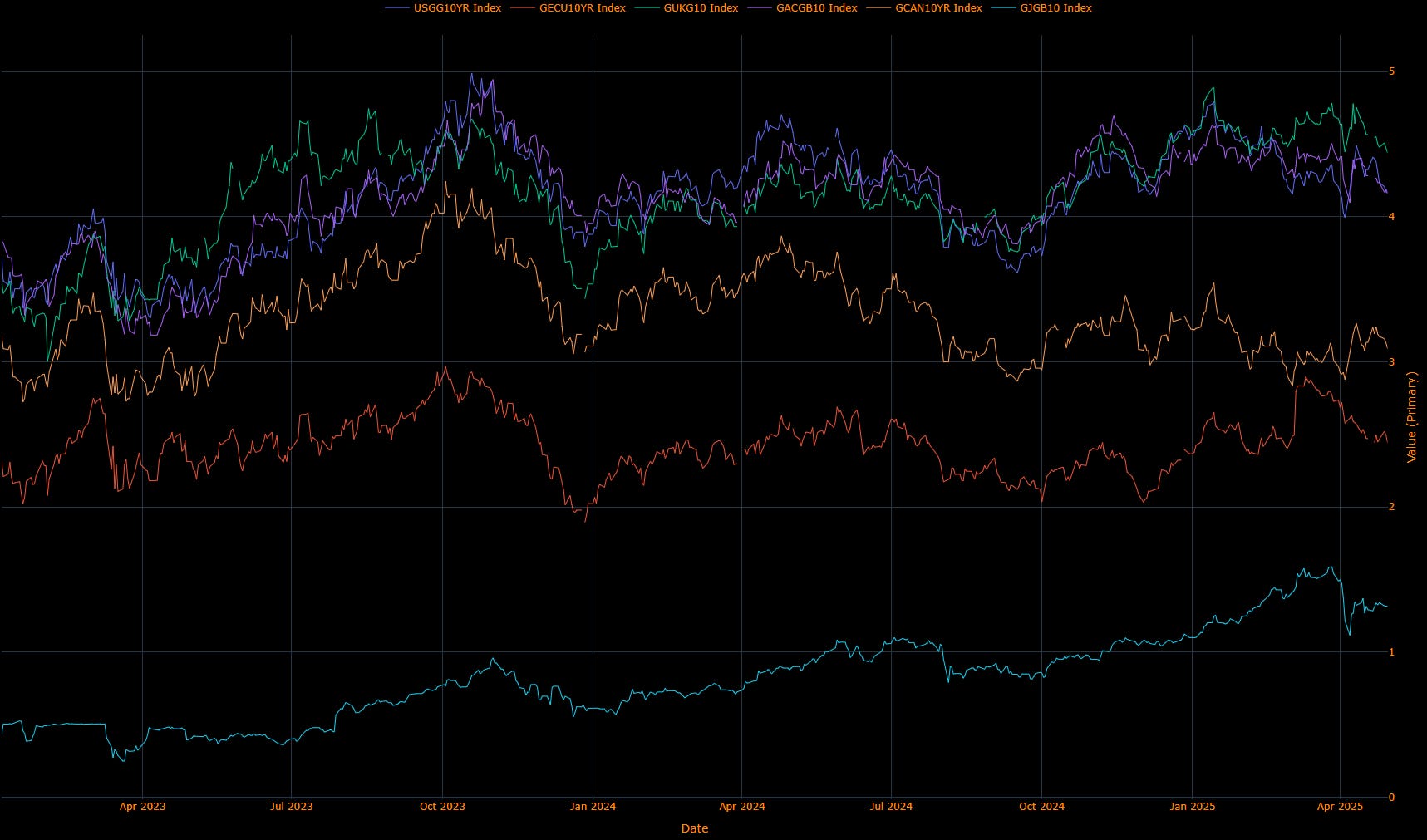

It’s been a tale of two (or three) worlds in bond markets. Interest rate developments are diverging sharply: the U.S. long end is selling off hard (yields up to multi-year highs) even as some other central banks are cutting rates. Here’s a snapshot of 10-year government bond yields across key regions:

A few big themes stand out:

U.S. Yields Soar: Despite the Fed pausing rate hikes, U.S. Treasury yields spiked in May. The 10-year yield blew past 4.5%, briefly kissing 4.6% last week. Even the 30-year yield hit 5.15% intraday – the highest since the October 2023 “debt scare” episode. What’s going on? In a word, fiscal worries. The Moody’s downgrade of U.S. debt underscored concerns about the $36 trillion debt pile and rising deficits. Investors are demanding a higher term premium to hold long-term U.S. bonds, especially with persistent inflation and heavy Treasury issuance. In essence, the bond market is flashing a bit of a warning to Washington: get the deficit under control or we’ll make borrowing costly. As a result, we’ve seen a steepening yield curve – remarkably, this is happening even as the Fed has already started cutting rates (the Fed cut 100 bps total in late 2024). The Fed’s policy rate is around 4.3% now, yet 10- and 30-year yields are well above that, pricing in inflation risk and less Fed support. From a trading perspective, I’ve been short duration on U.S. Treasuries – thankfully – because it’s been a bond bloodbath with prices falling as yields rise. I still think U.S. long yields could grind higher unless we get either a growth scare or some fiscal credibility restore. However, with 10s at ~4.5-4.6%, I’m not adding fresh shorts here; we’re at levels that could attract buyers if, say, recession odds increase. I am, however, selectively long some short-term U.S. paper – for instance, 2-year Treasuries yield around 4% and should be anchored if the Fed stays on hold or cuts next year. In fact, Fed expectations have shifted: the Fed held rates at 4.25–4.50% in the May meeting, and Fed officials (like Waller and Williams speaking this week) are hinting they’ll stay on hold for a while given tariff-driven price spikes. The Fed’s tone is cautious – they’re watching if these tariffs push up inflation (early evidence suggests yes, prices of imported goods are rising). I suspect the Fed will not cut further until there’s clear disinflation, so short-end yields might remain around current levels. Net result: I’m positioned for a continued U.S. curve steepening – effectively short long bonds, neutral/long short bonds. This stance paid off as the 30Y-5Y spread widened recently. I’ll adjust if we see any cooling in inflation or resolution in D.C. that could bring yields down.

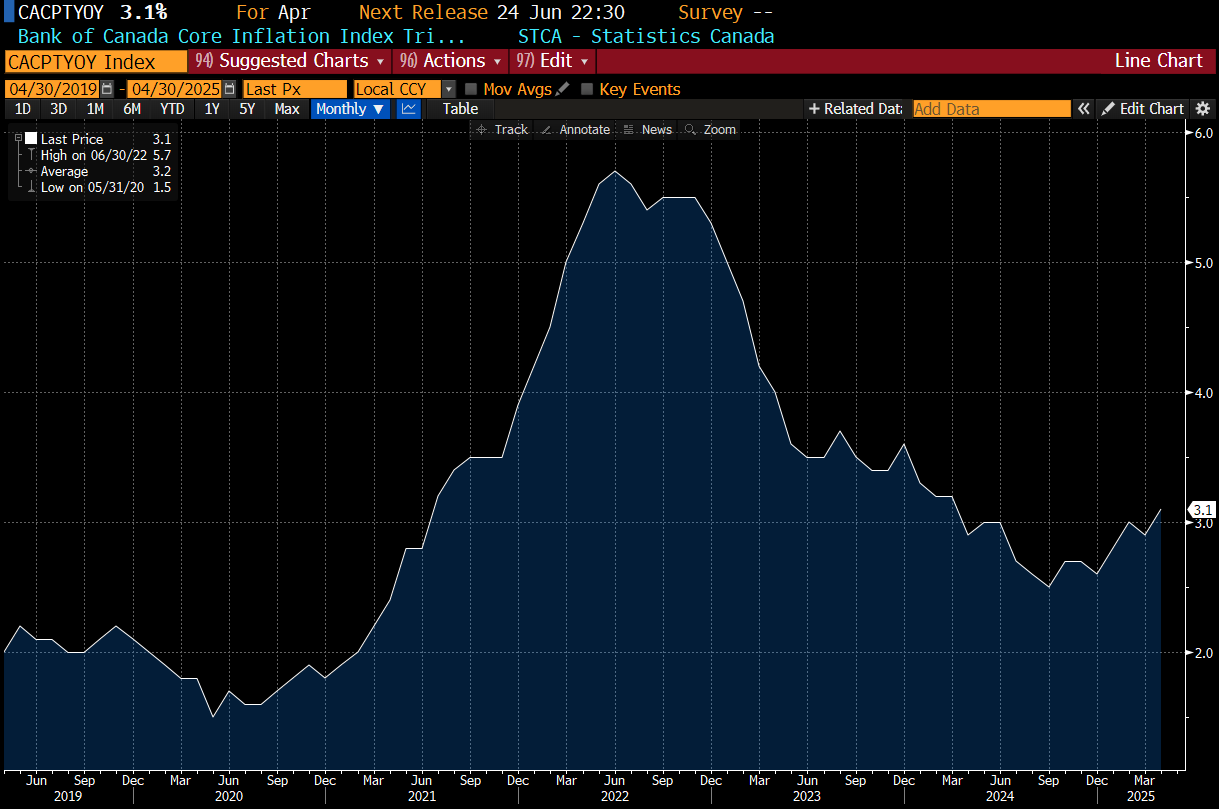

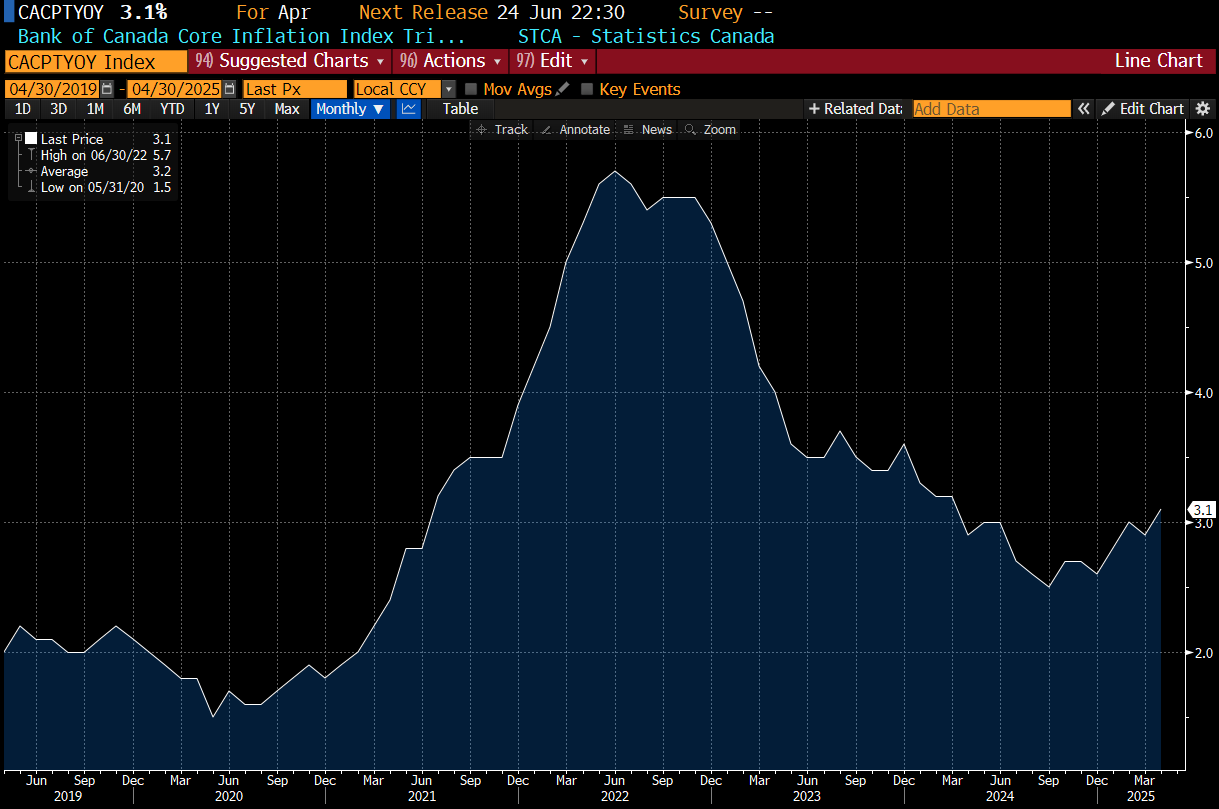

Canada – BoC Caught in a Bind: Canada’s bond yields have largely followed the U.S. (10-year at ~3.3% now, up from ~3.0% a month ago). The Bank of Canada has already been in easing mode – they cut earlier this year and the policy rate sits at 2.75%. In April, the BoC held rates steady, citing a need to gauge the impact of the U.S. trade war on Canada’s economy. The Canadian situation is tricky: headline inflation actually fell sharply to 1.7% in April (helped by a temporary scrap of the carbon tax on gas), but core inflation is sticky around 3%.

At the same time, the economy is showing cracks – unemployment ticked up to 6.9% as manufacturing took a hit from tariffs. The BoC is essentially stuck between a weakening economy and still-too-high core inflation. Markets earlier this month were pricing a high chance of a BoC rate cut in June, but after that firmer core CPI, those odds dropped (only ~35% chance of a cut now). My take: the BoC will likely hold at the June 4 meeting, emphasizing data-dependence. For trading Canadian rates, I’m not taking big positions – maybe a small long in 5-year Canada bonds, as I suspect if the trade war worsens or global growth slows, Canada will cut sooner or later (the market still prices cuts by year-end). One interesting dynamic: Canadian yields have moved in sync with U.S. Treasuries lately. If U.S. yields keep climbing, Canadian yields might too, but I suspect the spread could widen (Canada yields lower relative to U.S.) if BoC diverges dovishly from the Fed. I’m watching that spread; if U.S.-Canada yield differentials get too wide, it might present a trade (e.g. buy Canadian bonds vs short U.S. bonds).

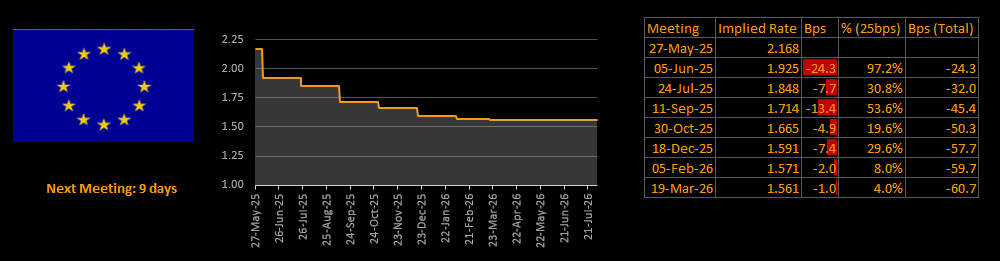

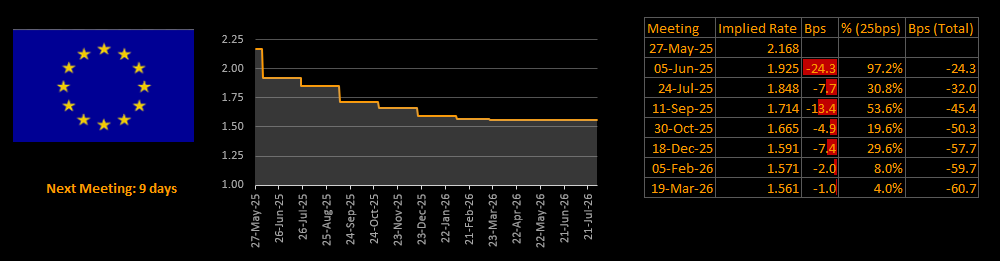

Eurozone – ECB Easing Underway: The ECB has pivoted from fighting inflation to supporting growth. In fact, they’ve cut rates seven times in the past year! Most recently in April, the ECB cut another 25 bps, bringing the deposit rate to 2.25%. This is the lowest since end-2022 and a clear reversal from the rapid hikes of 2022–23.

Why the change? Because the inflation spike has dissipated and growth is anemic. Eurozone headline inflation is ~2.2% as of April – basically right near the ECB’s target. Meanwhile, the economy is fragile (Eurozone Q1 GDP was around flat). The trade war is a big concern for Europe, which is more export-dependent. The ECB’s tone has turned dovish: President Lagarde noted “exceptional uncertainty” and even debated a larger 50 bps cut before settling on 25 bps, which was unanimous. Importantly, the ECB removed language about policy being “restrictive”; they’re clearly open to further easing if needed. Bond market reaction? European yields have fallen significantly from last year’s highs. The German 10-year Bund yield is ~2.56%, down from around 3% at the peak. When the ECB cut in April, euro yields dropped and the euro currency initially weakened, as traders anticipated more cuts ahead. (We’ll talk FX in the next section.) Eurozone peripheral bonds (like Italian BTPs) rallied too, as easier policy and ECB support reduce fragmentation risk. I have been long some European bonds (especially Italian 10-year) as a yield play, and that’s done well. However, it hasn’t been completely one-way – during the worst of the U.S. tariff scare, even German yields inched up briefly (safe-haven Bunds weren’t as robust because one of the “risks” was U.S. selling EU assets on tariff concerns). But broadly, the trajectory is down. My plan: stay long Eurozone duration selectively. I expect the ECB to potentially cut again in June or July, given their own forecasts show inflation falling to ~2% by 2025 and growth risks from tariffs. This week we’ll get flash May inflation for Europe’s big countries (Germany, France, etc.) – if those show inflation still tame (consensus is around 2% YoY), it will reinforce the ECB’s easing bias. One more thought: UK rates – the Bank of England also cut 25 bps recently amid tariff fallout and slowing UK growth. UK gilts have rallied on that move. I mention it because it highlights a global trend: outside the U.S., central banks are leaning dovish due to the trade war’s hit. That divergence (Fed on hold, others cutting) is key to my macro view.

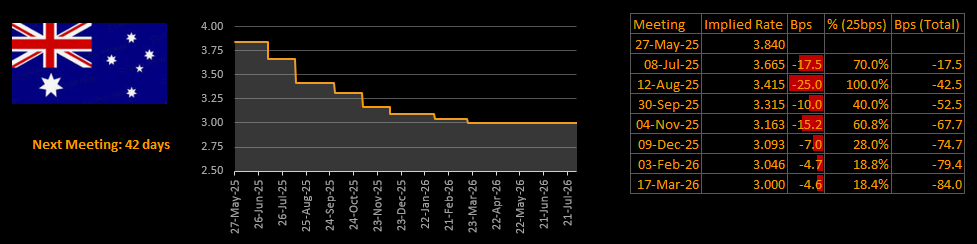

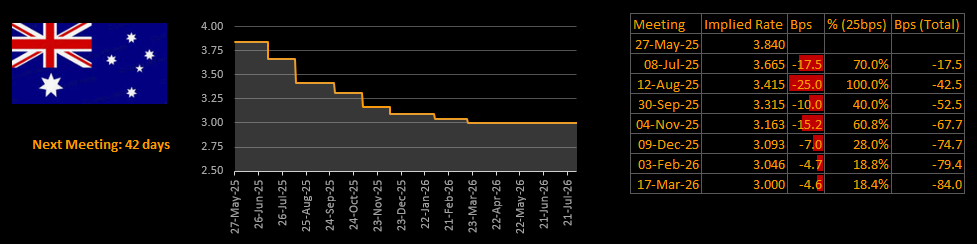

Australia – RBA Turns Dovish, Room to Rally: In a notable shift, the Reserve Bank of Australia cut rates on May 20 by 25 bps to 3.85%, a two-year low. Governor Michele Bullock explicitly cited Trump’s tariffs as a risk to Australia’s outlook.

With domestic inflation cooling and unemployment likely to rise due to global headwinds, the RBA felt it had scope to ease. They even discussed a 50 bps cut, showing they’re serious about supporting growth. The RBA statement noted that upside inflation risks have diminished and that policy is ready to respond “decisively” if global trade takes a severe downturn. Australian bond yields fell on the cut – the 3-year yield dropped (futures up 15 ticks on the announcement), and 10-year yields also came down from ~4% to the mid-3s. Market pricing implies more cuts ahead (about 60% chance of another cut by July). I agree: I think the RBA will cut again in coming months, given China’s slowdown and tariff impacts on Aussie export sectors (like agriculture, commodities). For trading, I like being long Aussie bonds – the curve could steepen if short rates fall further. Also, Australian rates are relatively high compared to other developed markets, so there’s room for yields to decline. One caveat: after the cut, the Australian dollar fell as Bullock sounded very dovish (more on FX later). That currency move actually helps Australia’s economy (more competitive exports), which could give the RBA some breathing room to not cut too fast. They seem to be opting for a “gradual and cautious” easing (similar to the BoE’s stance of gradual cuts). So I’m not expecting an aggressive slashing of rates, but a steady downward trend.

Japan – The End of Negative Rates, Yields Break Out: The Bank of Japan has finally begun normalizing policy after decades of ultra-ease. In January 2025, the BOJ raised its short-term policy rate to +0.5%, effectively ending the negative rate regime that had been in place (they’d been at -0.1% for years). They also scrapped the hard yield curve control cap on the 10-year (which was previously around 1.0%). This is huge: it means Japanese yields can trade more freely – and indeed, the 10-year JGB shot up to about 1.58% last week, the highest since 2008.

Why is the BOJ tightening? Inflation in Japan finally hit the target sustainably – core CPI has been ~3% for months, and wages are rising at their fastest in decades (3%+ wage growth). Governor Ueda has signaled that if inflation broadens, they will hike more. Markets expect another BOJ hike by Q3 (likely July). For global markets, this is a big deal: Japan was one of the last anchors of low yields. Now Japanese money may not flow out as much – domestic investors can get 1.5% at home risk-free, whereas before they’d buy U.S. Treasuries or Aussie bonds for yield. This shift could be contributing to upward pressure on yields elsewhere as well. In my trading, I haven’t done as much in JGBs (liquidity and BOJ intervention risk make it tricky), but I have kept an eye on Japanese yield movements as a barometer. Notably, despite rising JGB yields, the yen hasn’t strengthened much. Normally higher yields would boost a currency, but in Japan’s case, the yen remains mostly driven by risk sentiment and interest rate differentials with the U.S. – and U.S. yields have risen in tandem. So yen is soft (USD/JPY ~142-143), which ironically helps Japan’s economy a bit, perhaps allowing the BOJ to proceed slowly. Looking ahead, I anticipate the BOJ might hike once or twice more (maybe to 1.0% overnight by year-end), but they will be very cautious not to derail the economic recovery. For now, Japanese bonds have sold off (prices down, yields up) – foreign investors might even find 1.6% JGBs somewhat attractive if hedged, but I’m not playing in that pool yet.

Bottom line (Rates): We have a notable divergence: North America yields up, elsewhere yields down. My positioning reflects that: underweight U.S. duration (especially long-term), overweight European and Aussie duration. I also like some relative trades – e.g. long European bonds vs short U.S., which benefits if the divergence continues. The big risk to watch is inflation. If these tariffs keep pushing prices up (early evidence: U.S. manufacturing input prices had their biggest jump since 2022 due to tariff worries), central banks like the Fed could be hamstrung from cutting, which means yields might not fall even if growth slows. That is essentially stagflationary. However, I think many central banks (ECB, RBA, BoC) will prioritize growth and look through one-off tariff inflation. It’s the Fed and maybe BOJ that have the harder job because the U.S. inflation might re-accelerate while Japan’s is just hitting target. For the coming week specifically, FOMC minutes (Wednesday) will be parsed for how the Fed views the tariff impact on policy, and U.S. core PCE Friday will be crucial – a higher print could push long-end yields even further up. Also, Canada Q1 GDP on Friday will tell us if their economy stalled (forecast is basically zero growth); a weak number could cement BoC easing and rally Canadian bonds. I’ll be watching and ready to adjust duration if needed.

Commodities

Commodity markets have been sending mixed signals, reflecting the cross-currents of robust safe-haven demand versus fears of slowing growth.

Gold & Precious Metals – Shining Bright: It’s been gold’s time to shine. Gold prices rocketed to an all-time high, trading above $3,300/oz last week. That’s right – we blew past the old $2k level by a mile. The catalyst has been a potent combo of safe-haven flows and inflation hedging. When the U.S. credit rating got downgraded and fiscal deficit fears grew, investors flocked to gold as a store of value. Additionally, tariff turmoil raised worries about geopolitical risk and future dollar weakness – again gold benefits. I was long some gold into this (not gonna lie, partly as a hedge against my equity risk), and it paid off nicely. Gold hit a monthly high around $3,345 on Friday before pulling back a bit. It did retrace some gains late week as immediate haven demand ebbed (with the tariff delay news), but it’s still holding in the $3,200s. I remain bullish on gold medium-term. Central banks (especially in Asia) have been buying gold reserves, and the looming U.S. fiscal issues make the dollar’s long-term outlook a bit murkier – gold is an attractive alternative. That said, after such a sprint, I wouldn’t be surprised to see some consolidation. If we get any progress on trade deals or stronger economic data, gold might dip. I’d view dips as buying opportunities unless something fundamentally changes. Interestingly, platinum outperformed even gold last week – up over 11%. That was partly on a flurry of supply issues and short-covering. I’m not as involved in platinum, but its surge confirms that precious metals are broadly bid.

Oil – Under Pressure from OPEC+ Moves and Tariffs: Crude oil has been struggling. We’re looking at Brent crude around $64-65/barrel, which is the lower end of its range of the past year. In the last few weeks, oil actually fell further (down ~5% since early May). The primary reason: oversupply concerns. OPEC+ has been increasing output – a sharp turnaround from the production cuts of 2022. In fact, there’s talk that at the upcoming June 1 meeting, OPEC+ will announce another large output hike (possibly +411,000 barrels/day for July). A Bloomberg report on May 22 suggested as much, and oil prices promptly dropped on that speculation. It seems key producers (maybe Saudi, Russia) are prioritizing market share over price. Additionally, we saw U.S. crude inventories unexpectedly rise, indicating weaker demand or at least adequate supply. On top of supply factors, the demand outlook is clouded by the trade war – if global growth slows or if China’s economy stumbles, that’s obviously bearish for oil. From a trading standpoint, I’ve been moderately bearish on oil since it broke below $70. I continue to hold a small short bias (via puts on oil ETFs). The rationale: until I see either OPEC reversing course or evidence of a strong pickup in demand, it’s hard for oil to rally. One wildcard – if the U.S. economy holds up better than feared (some recent data like retail sales have been okay) and if China’s stimulus kicks in, oil could find a floor. Also, there’s always geopolitical risk (Middle East tensions, etc.) that can cause a price spike. But for now, the path of least resistance seemed down, and indeed we touched multi-month lows. In the coming week or two, I’ll watch that OPEC+ meeting outcome closely – if they do go for another output hike, that could keep oil in the low-$60s. On the flip side, any hint that OPEC is uncomfortable with sub-$60 prices and might cut later could trigger a short-covering rally. So I’m nimble, but leaning bearish until proven otherwise.

Base Metals & Others: Industrial metals like copper and iron ore have been sluggish, echoing the growth concerns. Copper is off its highs, trading around ~$4.00/lb (well below last year’s peaks). Iron ore – important for Australia – has languished under $100/tonne. The tariffs haven’t directly hit these (since they’re more raw materials), but the indirect effect is expected weaker demand. However, I note a bit of optimism creeping in: if China does deploy stimulus, it usually involves infrastructure (which would boost metal demand). That’s perhaps why these markets didn’t collapse outright. I have a small long position in copper as a speculative play on a China rebound, but it’s a bit contrarian. Agricultural commodities also saw a lift in late May: weather issues (droughts, etc.) and the Black Sea tensions have pushed grain prices up. Hedge funds reportedly piled into grains ahead of key crop reports. I’m not heavily in ags, but I keep an eye since food price inflation can feed into central bank thinking.

In summary, commodities are reflecting a hedged bet: precious metals are pricing in the turmoil (and inflation risk), while oil and base metals are pricing in slowdown. My playbook is to stay long the former (gold especially) and cautious on the latter. This week, keep an eye on Chinese PMI data (May 31) – a weak number could pressure metals/oil further, while a surprise uptick might give them a bounce. Also, any new talk of strategic oil reserve buys or OPEC surprises could jolt crude.

Currencies

The foreign exchange market has seen the U.S. dollar slip back from its highs, as interest rate differentials and risk sentiment shift. I’ll go through the major currencies in our focus regions:

U.S. Dollar (USD): After spending much of the past year strong, the USD has started to retreat broadly in recent weeks. The Dollar Index (DXY) is off its highs, largely because markets are sensing the Fed is done hiking (while other central banks are still active) and because U.S. deficits are raising eyebrows. When U.S. equities wobbled mid-May, the dollar initially caught a safe-haven bid briefly. But notably, as the dust settled, the dollar actually fell alongside U.S. stocks – suggesting investors might be questioning U.S. assets a bit more fundamentally. I’ve noticed this correlation flip: normally “risk off” means dollar up, but with the **tariff-driven inflation and fiscal issues, the dollar has been soft even on equity down days. My interpretation is that the huge U.S. twin deficits (budget and trade) are finally weighing on the buck. In fact, BlackRock pointed out that investors are demanding more compensation (yield) to hold U.S. bonds due to deficits, and historically such episodes have seen the dollar weaken while U.S. term premiums rise. That’s exactly what’s happening. So I’ve turned mildly bearish on USD for the near term.

EUR/USD: The euro has been one of the biggest gainers against USD. EUR/USD broke above 1.14 to finish last week at its highest level of the year. It got an extra boost when Trump postponed the EU tariffs, which removed a big cloud – the euro popped on that news to around $1.139 on Monday. Part of euro strength is also the narrowing rate gap: Fed is on hold, ECB is cutting but slower, and importantly U.S. long yields are up (which could eventually hurt U.S. growth) whereas Europe’s situation might improve with China stimulus and no domestic trade war. I have been long EUR/USD since it was in the mid-1.12s, adding on dips. I still like it, though it’s had a run. I think diversification away from USD by global investors (some due to U.S. unpredictability in policy) could support the euro. Near term, we’ll watch European inflation data – if Eurozone CPI (flash) comes in soft, it might paradoxically weaken the euro a bit (since ECB might cut more). But I suspect the bigger driver is market risk appetite and U.S. developments. For now, euro’s holding gains – up roughly 2% over the past week against USD. I’ll stay long but perhaps take partial profits if we approach 1.15-1.16, which could be technical resistance.

Japanese Yen (JPY): Usually the yen rallies in times of turmoil, but this time it “remained soft” despite volatility. As noted, USD/JPY is around 142-143 yen per dollar, which is actually weaker yen than a month ago (it was in the high 130s in April). Why isn’t yen acting as a safe haven? Two reasons: interest rate differentials and Japan-specific trade fears. U.S. yields jumped, making USD assets more attractive to yield-seekers, while Japan’s yields, though rising, are still low – so the rate gap still favors the USD. Also, Japan is itself exposed in the trade war (if U.S. tariffs hit autos, Japan gets hurt), so the yen isn’t a pure safe haven in a U.S.-centric conflict. In fact, when tariffs worries hit, some may have sold yen anticipating BOJ will stay easy to support the economy. I had expected yen to do a bit better, but I was cautious given these factors, so I wasn’t heavily long yen as I might have been in another risk-off scenario. Going forward, I actually see some potential for yen strength if global risk worsens significantly or if U.S. yields peak. But for now, momentum favors USD/JPY upside (yen weakness). I’ll possibly look to short USD/JPY around 145+ if it gets there, as I think the BOJ would become uncomfortable and perhaps intervene if yen weakens too much (they did in 2022 when USD/JPY went above 150). For the coming week, watch Japan’s economic data (Tokyo CPI, retail sales) – strong numbers could fuel speculation of another BOJ hike, which might give the yen a lift. Conversely, continued market calm with high U.S. yields could keep USD/JPY grinding up.

British Pound (GBP): Briefly, the pound has quietly firmed against USD, trading near $1.28. The Bank of England’s cut didn’t crush the pound; in fact, the BoE’s “gradual cuts” guidance made traders think the BoE won’t aggressively ease, supporting GBP. Plus, the weaker dollar narrative helps. I’m not focusing heavily on GBP in this report (UK not a main region asked), but I maintain a mild long bias on GBP/USD, targeting 1.30, as long as risk sentiment and the USD trend allow.

Canadian Dollar (CAD): The loonie has had a choppy ride. In early May, USD/CAD spiked to ~1.393 (CAD weakest in 3 weeks) when broad USD strength returned and the BoC highlighted trade war risks. Essentially, when the Fed sounded a bit hawkish (Powell said no hurry to cut more) and the trade war escalated, the USD got a bid and CAD, being a pro-cyclical currency, fell. But since mid-May, the CAD has clawed back some gains as the USD softened broadly. By this week, USD/CAD is hovering around the mid-1.37s. The CAD got some relative support from the fact that Canada was not directly hit by new U.S. tariffs (beyond existing metals tariffs) – one strategist noted CAD outperformed other commodity currencies because Canada was “relatively shielded” from the latest tariff round. Also, any uptick in oil at times or strong domestic data (Canada retail sales jumped one day, giving CAD a boost) helps. That said, CAD’s upside is capped by the dovish BoC and soft commodity prices. My positioning on CAD is modest – I was long CAD earlier when it dropped (short USD/CAD) on the view that the tariff exemption would help, but I took profit as it rebounded. At ~1.37-1.38 USD/CAD, I’m neutral. If oil were to mount a sustained rally or if U.S. data weaken (hurting USD), I’d expect CAD to strengthen (USD/CAD back toward 1.34–1.35). Conversely, if global risk-off hits again, CAD could be vulnerable (it’s high beta). For now, I’ll watch Canada’s GDP and any BoC speak for cues.

Euro crosses / others: Given the focus regions, one interesting cross is EUR/JPY – it’s been rising with euro strength and yen weakness, reaching multi-year highs. Also, AUD/USD I should mention: the Australian dollar is actually at its highest level of 2025 now, around $0.65–0.66. It was buoyed by the improved risk mood and optimism on China, even despite the RBA’s dovish cut. In fact, after initially dipping on the RBA move (AUD fell to ~$0.642), it roared back as trade tensions ebbed and commodity currencies rallied. I’m long a bit of AUD/USD from ~0.645, riding this momentum. I have to be careful since AUD is highly sensitive to both China news and global stock swings. But with RBA easing and China stimulus on deck, it could continue to grind higher. EUR/AUD might also be interesting – two relatively strong currencies; I suspect range-bound there.

A few other FX observations: Norway’s krone was the top G10 performer last week – likely helped by a relief in risk sentiment and perhaps positioning (it had been very weak, so it bounced hard). I mention this because it shows the pattern: commodity and smaller currencies jumped when the USD slipped. The dollar retreat has been the big FX story. Meanwhile, emerging market currencies (not our main focus, but worth noting) have had some relief too. The Chinese yuan (offshore CNH) had weakened on trade escalation, but steadied around 7.1 per USD after China signaled support measures – this helped AUD as mentioned.

Bottom line (FX): I’m positioning for a continuation of the dollar softening trend, but not in a straight line. I like euros and AUD against USD, and I’m cautious on JPY until I see a catalyst for a reversal. Risk events ahead that I’m watching: U.S. PCE and GDP (if these surprise high/strong, USD could get a short-term bounce as rate cut bets get priced out). Also, any Fed speak hinting at concern over dollar weakness (unlikely, but worth listening). And of course, any further tariff news – if Trump were to fully rescind the threatened EU/China tariffs, I’d expect a risk rally and possibly further USD selling (as safe-haven demand falls). Conversely, if tariffs come back full force in July, that could be a dollar-positive risk-off (though as discussed, even that is not guaranteed to boost USD like before). It’s a nuanced FX environment, but the trend of 2025 so far is away from the peak dollar of ’22–’23.

To wrap up, markets are digesting a unique mix of factors: a potential trade war (version 2.0) emanating from the U.S., central banks pivoting to support growth, and fiscal stresses rearing their head. My approach going into this week is to stay nimble and hedged. I’ve got my core convictions (long-quality equities, long gold, short U.S. long bonds, long EUR/AUD, etc.) but I’m ready to adjust if the narrative shifts. The upcoming week has some critical items: tech earnings, U.S. core PCE inflation, FOMC minutes, and China PMI. Any one of these could be a market mover:

If Nvidia’s earnings (Wednesday) blow past expectations and guide strong, it could reignite another tech rally – good for equities broadly.

If core PCE (Friday) shows an accelerating trend (due to tariffs or otherwise), it might spook bond traders even more and force a reassessment of Fed trajectory, boosting yields and possibly jolting stocks.

The FOMC minutes will likely show how the Fed is viewing the tariff situation – I expect them to emphasize uncertainty and willingness to act if needed. Any hint of discomfort with inflation could be read hawkishly.

China’s NBS PMI (Saturday) will give the first real look at post-tariff manufacturing sentiment in China. A very weak number could increase global growth fears (negative for equities/commodities, positive for bonds/possibly USD), whereas a stable number might reassure that the world’s second-largest economy isn’t tanking.

On top of that, we’ll hear from various central bankers (Fed speakers like Williams, ECB speakers, etc.) and get data like Eurozone confidence, Germany CPI, Canada GDP, as noted. With U.S. and UK markets having been closed Monday, liquidity is a bit thinner this week, which could exaggerate moves. So I’m mentally prepared for some whipsaw.

In sum, I’m entering the week cautiously optimistic – I think the worst of the trade fear may be priced in for now (given the tariff delays), and underlying economies (especially U.S.) are proving resilient enough so far. But I have no illusions: headlines or surprises can change everything. My portfolio is balanced, with hedges like gold and put options to protect against downside risk, and I’m ready to tweak exposure as new information comes in. That’s the life of a macro trader – keep one eye on the data, one eye on the tweet feed, and stay flexible. Here’s to a (hopefully) quieter, but profitable, week ahead!